At Home Owners Association, we understand the desire to break free from mortgage debt sooner. Owning your home outright is a significant milestone that can provide financial freedom and peace of mind.

This blog post will explore practical tips to pay off your home loan faster, helping you achieve your goal of early homeownership. We’ll cover strategies ranging from making extra repayments to refinancing options and budgeting techniques.

How Extra Repayments Accelerate Your Mortgage

Extra repayments stand out as one of the most potent strategies to pay off your home loan faster. This approach reduces the principal balance and slashes the overall interest paid throughout the loan’s lifetime.

Automate Additional Payments

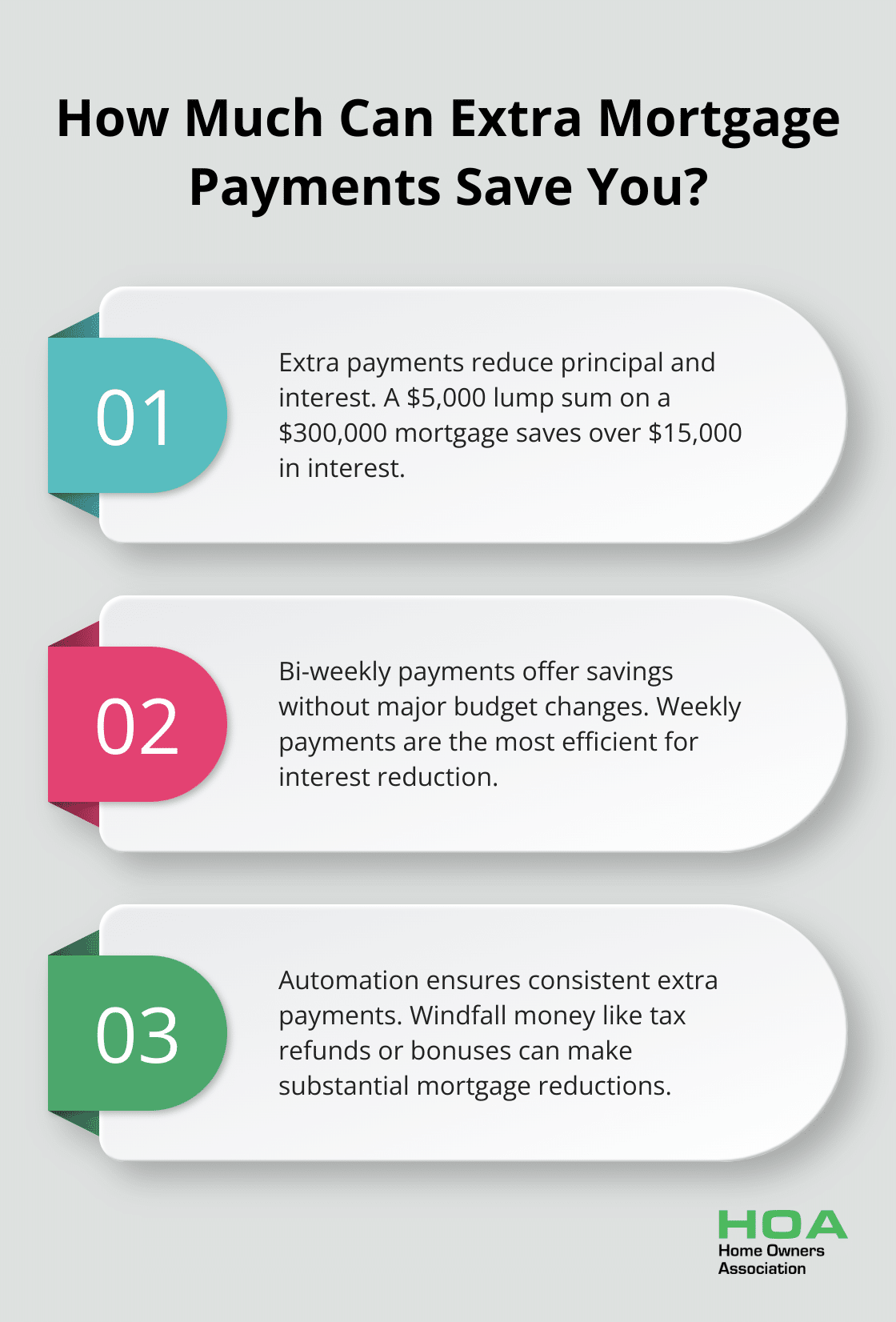

Automation of additional payments provides a foolproof method to consistently reduce your mortgage. Find out how much you can save when you make extra payments regularly, or if you make a one-off lump sum repayment into the home loan or mortgage. Contact your lender to establish this arrangement, ensuring the extra payments directly reduce the principal.

Use Windfall Money Wisely

Unexpected financial windfalls offer excellent opportunities to make substantial reductions in your mortgage. Tax refunds, work bonuses, or inheritances can dramatically impact your loan when allocated wisely. For example, a one-time payment of $5,000 on a $300,000 mortgage could save you over $15,000 in interest (and reduce your loan term by more than a year).

Opt for Bi-Weekly Payments

A simple change in payment frequency from monthly to bi-weekly can lead to savings without drastically altering your budget. Bi-weekly saves money albeit a small amount. Weekly is the most efficient. Interest is based off balance at time of payment.

Check for Potential Fees

It’s crucial to note that some lenders charge fees for additional payments or changes in payment structures. Always verify with your lender about any potential costs before implementing these strategies. Many Home Owners Association members have successfully negotiated with their lenders to waive such fees, highlighting the long-term benefits of faster loan repayment.

Maintain Consistency

Consistency proves key when making extra repayments. Even small, regular additional contributions compound over time, leading to substantial savings and bringing you closer to owning your home outright.

As we explore ways to accelerate mortgage repayment, it’s worth considering another powerful strategy: refinancing your home loan. This approach can potentially unlock even more savings and further speed up your journey to full homeownership.

Refinancing Your Home Loan: A Strategic Approach

Refinancing your home loan can transform your mortgage repayment strategy. This approach potentially reduces interest rates and shortens loan terms, accelerating your path to full homeownership.

Hunt for Competitive Interest Rates

The first step in refinancing involves a thorough search for better interest rates. The Australian Bureau of Statistics reported new borrower-accepted finance commitments for housing loans in February 2025. If your current rate exceeds the market average, substantial savings await through refinancing.

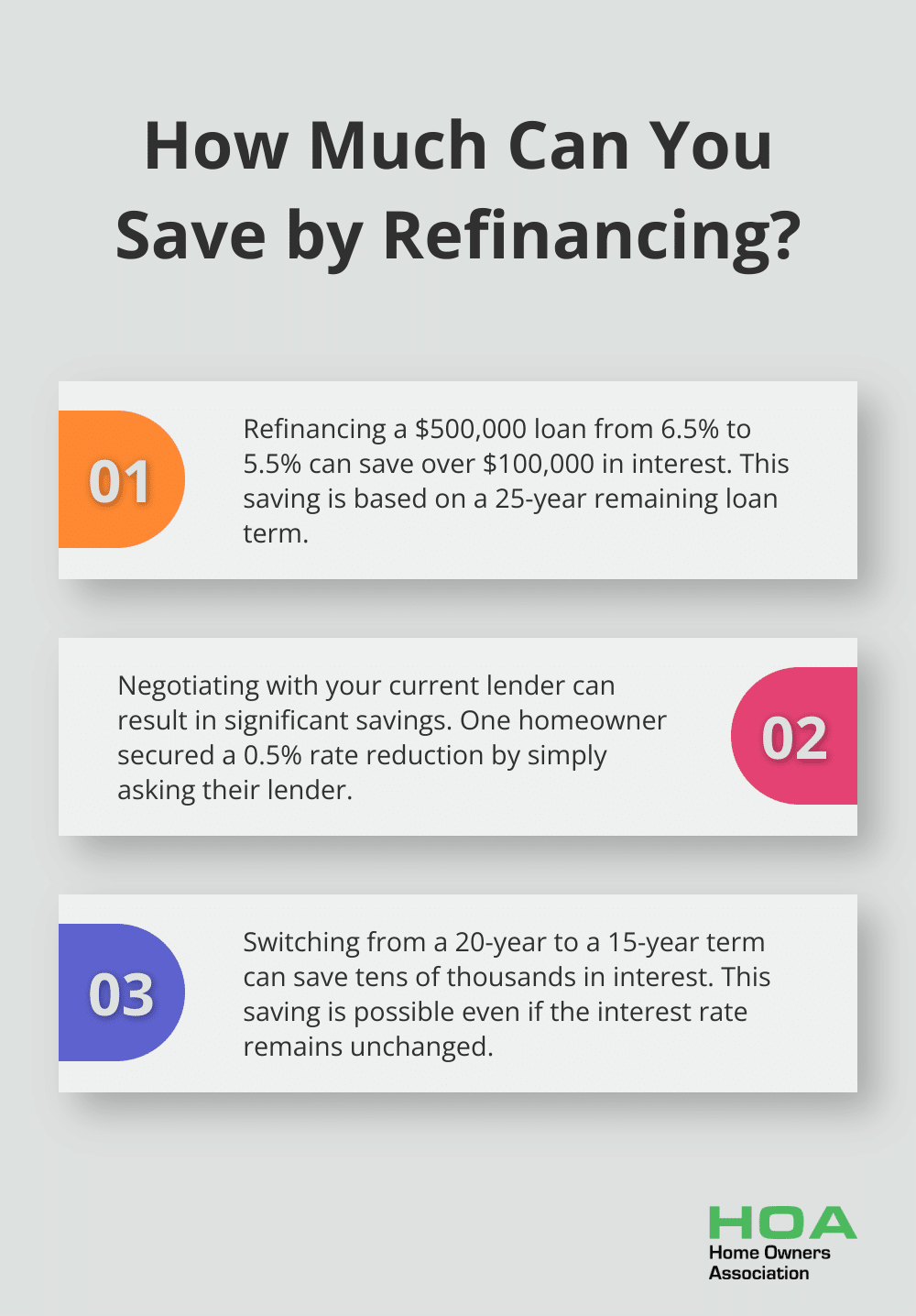

Consider this scenario: A $500,000 loan with 25 years remaining at 6.5% interest. A reduction to 5.5% could save over $100,000 in interest over the loan’s lifetime. (This extra cash could fuel additional repayments, further accelerating your loan payoff.)

Negotiate with Your Existing Lender

Before switching lenders, attempt to negotiate with your current provider. Many lenders employ retention teams specifically to retain valuable customers. Present competitive offers from other lenders and request a match or better deal.

A recent success story involved a homeowner who secured a 0.5% rate reduction simply by asking their lender. This straightforward conversation resulted in thousands of dollars saved without the hassle of changing lenders.

Consider a Shorter Loan Term

When refinancing, evaluate the option of a shorter loan term. While this choice might increase your monthly payments, it significantly reduces the total interest paid over the loan’s life.

For example, refinancing from a 20-year remaining term to a 15-year term could save tens of thousands in interest, even if the interest rate remains unchanged. (Ensure the higher payments comfortably fit within your budget before proceeding.)

Calculate the Break-Even Point

Refinancing isn’t free. You’ll likely encounter fees for ending your current loan and establishing a new one. Calculate the break-even point to ensure the savings outweigh the costs. If you plan to stay in your home for several more years, refinancing often proves a smart financial decision.

Explore Fixed vs Variable Rates

When refinancing, you have the option to choose between fixed and variable rates. Fixed rates offer stability and predictability, while variable rates might start lower but fluctuate with market conditions. Your choice depends on your risk tolerance and financial goals.

As you contemplate refinancing options to accelerate your mortgage repayment, it’s equally important to examine your overall financial picture. The next section will explore strategies to reduce expenses and increase income, providing additional resources to funnel towards your home loan.

Maximize Your Budget for Faster Loan Repayment

Create a Lean Budget

The first step to free up extra cash for your mortgage involves the creation of a comprehensive budget. Create a lean budget by considering options such as opening an offset account, making more frequent repayments, making extra repayments, evaluating fixed versus variable rate loans, and looking at ways to cut back.

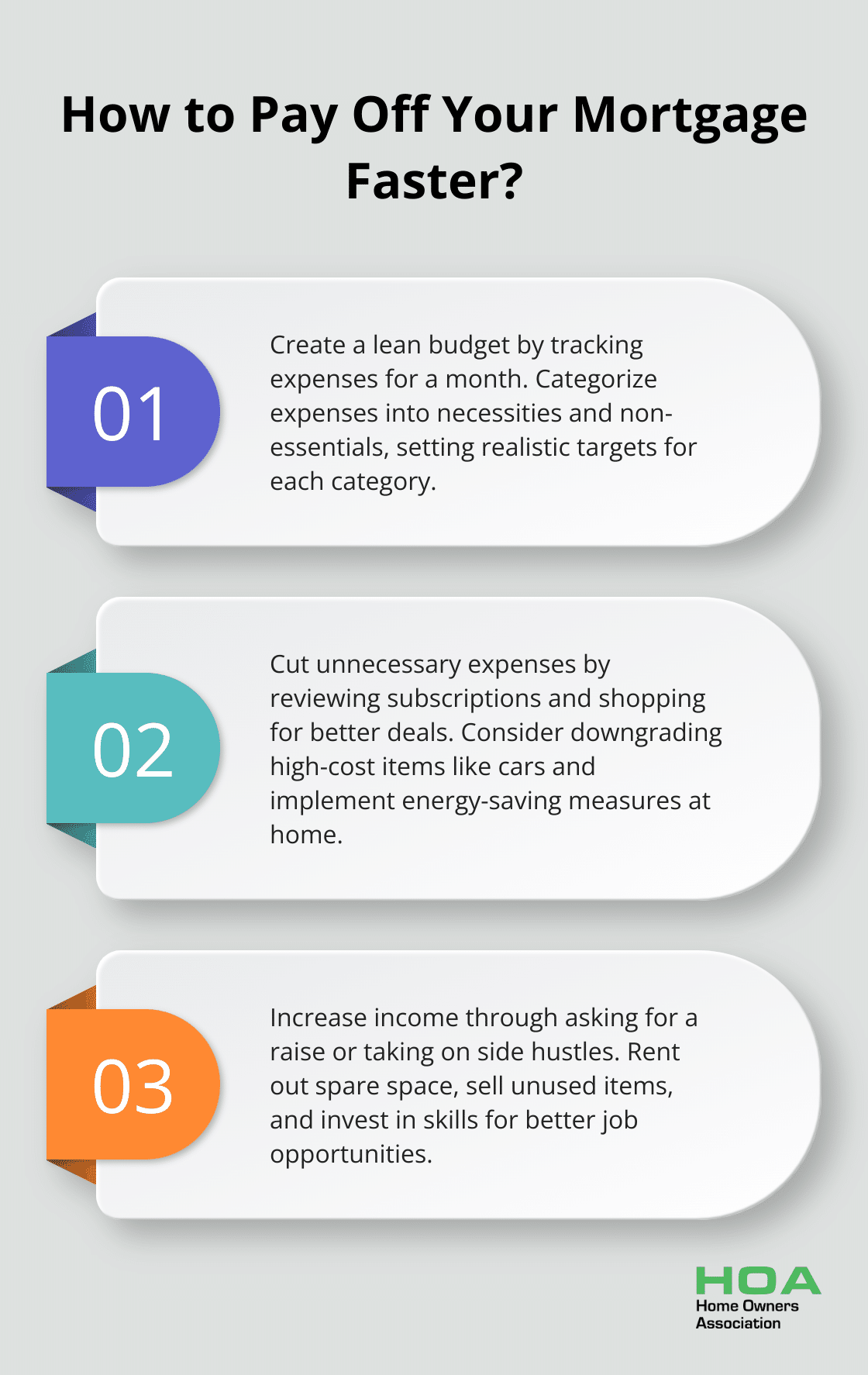

Start by tracking all your expenses for a month. This includes everything from your morning coffee to your monthly streaming subscriptions. Once you have a clear picture of your spending habits, categorize your expenses into necessities and non-essentials.

Set realistic targets for each category. You might reduce your dining out expenses or your entertainment budget. The key is to find a balance that allows you to maintain a good quality of life while freeing up funds for your mortgage.

Cut Unnecessary Expenses

Now that you have a budget, scrutinize your expenses and eliminate unnecessary costs. Here are some practical ways to reduce your spending:

- Review your subscriptions and cancel those you rarely use.

- Shop around for better deals on your utilities, insurance, and phone plans. Comparison websites can help you find the best rates.

- Consider downgrading your car if you have high car payments. A less expensive vehicle could free up a significant amount each month for your mortgage.

- Implement energy-saving measures in your home. Simple changes like using LED bulbs and improving insulation can lead to substantial savings on your energy bills.

- Plan your meals and grocery shopping to reduce food waste and impulse purchases.

Cut unnecessary expenses by taking stock of your income, expenses and savings, creating a budget to ensure you can manage future home loan repayments, and paying down outstanding debts.

Increase Your Income

While cutting expenses is important, increasing your income can have an even more significant impact on your ability to pay off your mortgage faster. Here are some strategies to consider:

- Ask for a raise at work. If you’ve performed well and haven’t had a salary increase recently, it might be time to negotiate. Prepare a case showcasing your value to the company.

- Take on a side hustle. The gig economy offers numerous opportunities to earn extra income. Whether it’s freelancing in your field of expertise or driving for a ride-sharing service, even a few hours a week can make a difference.

- Rent out a spare room or parking space. You can easily monetize unused space in your home with various platforms.

- Sell items you no longer need. This action not only declutters your home but also provides a cash injection for your mortgage.

- Invest in your skills. Taking a course or obtaining a certification could lead to better job opportunities or promotions, increasing your earning potential.

Every extra dollar you earn or save can go towards your mortgage, bringing you closer to financial freedom. The combination of these strategies with refinancing options will put you on the fast track to paying off your home loan.

Final Thoughts

Paying off your home loan faster requires a combination of strategies and unwavering commitment. Extra repayments, refinancing options, and budget optimization all play a role in reducing your mortgage term and interest payments. The real power lies in maintaining these habits consistently over time, as every additional dollar towards your mortgage decreases the principal and future interest.

Early loan repayment offers benefits beyond outright home ownership, including financial freedom, reduced stress, and opportunities for future investments. Your journey to faster home loan repayment will depend on your unique financial situation, goals, and risk tolerance. We at Home Owners Association support Melbourne homeowners throughout their property ownership journey with resources, guidance, and benefits to maximize home investments.

Applying these tips to pay off home loan faster doesn’t just eliminate debt-it invests in your future financial well-being. Start today and stay committed to your goal of early homeownership. (You’ll be amazed at how quickly your dream can become a reality with the right approach and determination.)