Choosing the right home mortgage can be overwhelming, but it’s a critical step in your homeownership journey. At Home Owners Association, we’ve compiled essential home mortgage tips to help you navigate this complex process.

Our guide will break down different types of mortgages, key factors to consider, and strategies for comparing offers. By understanding these elements, you’ll be better equipped to make an informed decision that aligns with your financial goals and circumstances.

What Are the Main Types of Home Mortgages?

Choosing the right home mortgage is a critical step in your homeownership journey. This guide breaks down different types of mortgages, key factors to consider, and strategies for comparing offers. You’ll be better equipped to make an informed decision that aligns with your financial goals and circumstances.

Fixed-Rate Mortgages: Stability in Uncertain Times

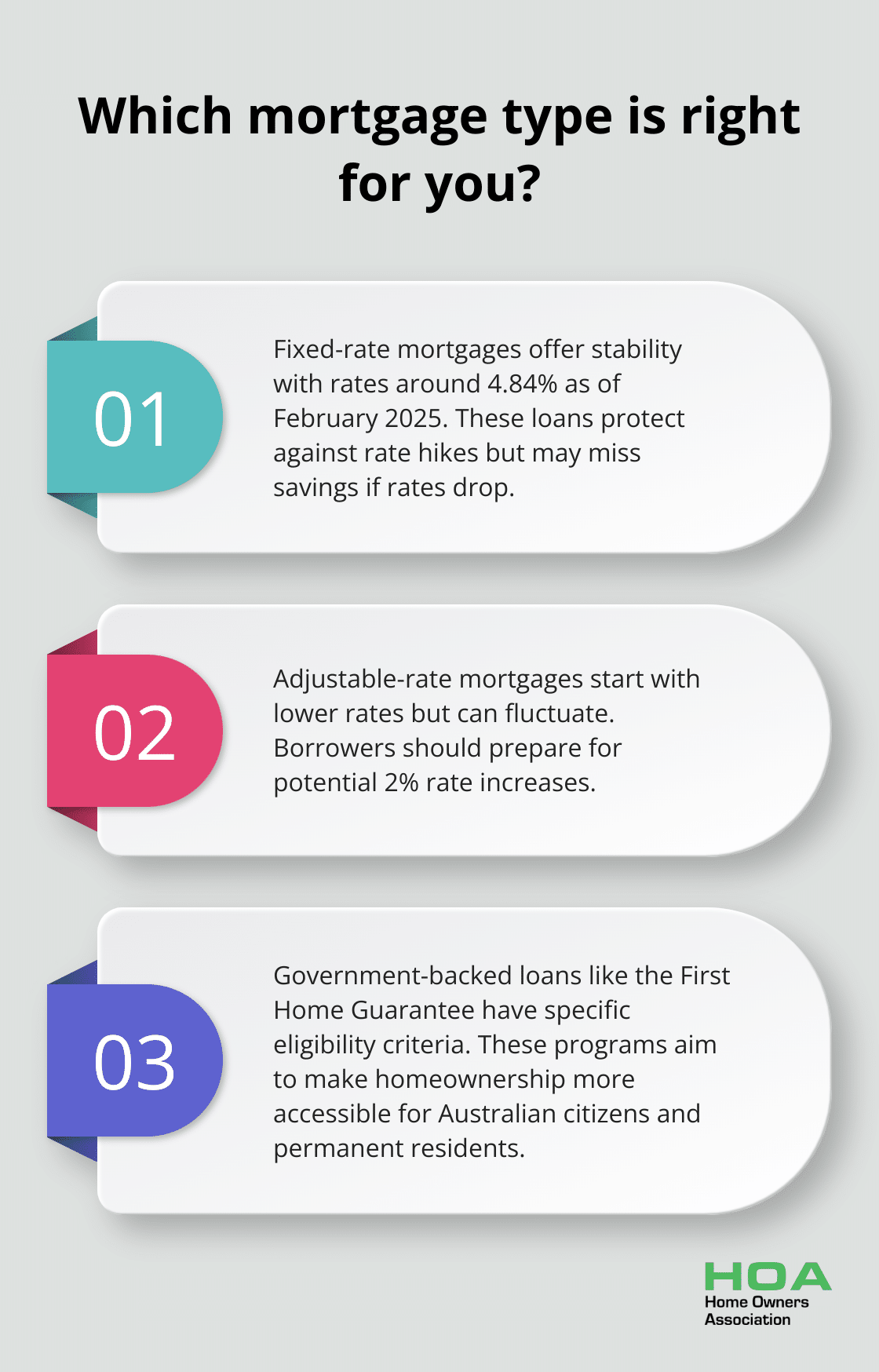

Fixed-rate mortgages are a popular choice for many Australians, especially in today’s fluctuating economic climate. With this type of loan, your interest rate remains constant for a set period (typically between one to five years). This means your repayments stay the same, which makes budgeting easier and protects you from interest rate hikes.

According to the Reserve Bank of Australia, as of February 2025, the cash rate stands at 4.10%. This has led to fixed-rate mortgages being offered at around 4.84% (comparison rate 5.92%). While these rates may seem attractive, you might miss out on potential savings if interest rates drop during your fixed term.

Adjustable-Rate Mortgages: Flexibility with Risks

Adjustable-rate mortgages (ARMs), also known as variable-rate mortgages in Australia, offer more flexibility but come with increased uncertainty. Your interest rate can fluctuate based on market conditions, which means your repayments can go up or down.

ARMs often start with lower interest rates compared to fixed-rate mortgages, making them attractive to first-time homebuyers or those who plan to sell or refinance within a few years. However, you should prepare for potential rate increases. You should ensure you can afford repayments if rates increase by 2%.

Government-Backed Loans: Accessible Options for Eligible Borrowers

In Australia, several government-backed loan programs aim to make homeownership more accessible. These programs often have specific eligibility criteria, such as being an Australian citizen or permanent resident at the time of entering the loan.

Other government initiatives include the Family Home Guarantee and the Regional First Home Buyer Guarantee. These programs can be game-changers for those who struggle to enter the property market, but they often come with specific eligibility criteria and property value caps.

Jumbo Loans: For High-Value Properties

Jumbo loans are designed for properties that exceed the conforming loan limits set by regulatory bodies. In Australia, these are often referred to as non-conforming loans. They typically come with stricter credit requirements and higher interest rates due to the increased risk for lenders.

If you’re eyeing a premium property in a high-cost area like Sydney or Melbourne, you might need to consider a jumbo loan. However, you should prepare for more stringent approval processes and potentially higher down payment requirements.

The key is to align your choice with your financial situation, future plans, and risk tolerance. You should compare offers from multiple lenders and consider seeking advice from a mortgage broker to ensure you’re getting the best deal for your unique circumstances. Now that we’ve covered the main types of home mortgages, let’s explore the factors you should consider when choosing the right mortgage for you.

What Factors Shape Your Mortgage Choice?

Interest Rates and Comparison Rates: The True Cost

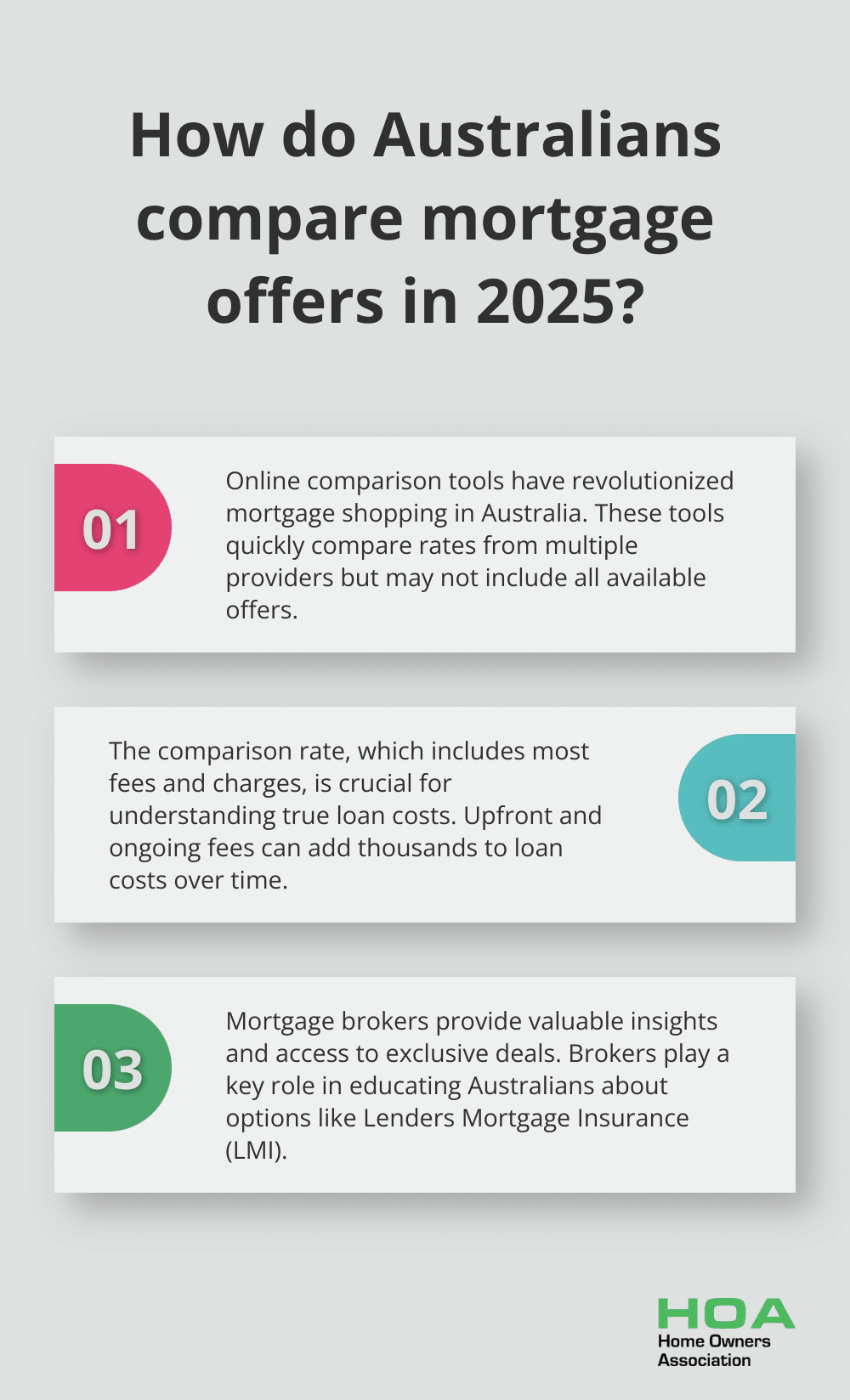

Interest rates catch the eye, but they tell only part of the story. The comparison rate includes both the interest rate and most fees and charges relating to a loan, providing a more accurate picture of the true cost. As of March 2025, home loan rates can be as low as 4.84%, with a comparison rate of 5.92%. This difference underscores the importance of looking beyond the advertised rate when selecting a mortgage.

Loan Term: Short vs. Long-Term Financial Impact

The length of your loan term significantly affects your total repayments. A 30-year term might offer lower monthly payments, but you’ll pay substantially more in interest over time. For instance, on a $500,000 loan at 4.84%, choosing a 25-year term instead of 30 years could save you over $64,000 in interest (despite higher monthly repayments).

Down Payment and LMI: Upfront Costs Matter

Your deposit size impacts not just your initial borrowing but ongoing costs too. In Australia, loans with a loan-to-value ratio (LVR) greater than 80% typically require Lenders Mortgage Insurance (LMI). This can add thousands to your loan. The First Home Guarantee scheme allows eligible buyers to secure loans with just a 5% deposit, potentially saving on LMI. However, this scheme has limited applications, so timing is key.

Hidden Costs and Fees: The Devil in the Details

Application fees, ongoing fees, and other charges can quickly accumulate. Industry data suggests these fees can exceed $40,000 for new home buyers (excluding interest and deposits). Always request a full breakdown of fees and consider how they impact the total cost of your loan over its lifetime.

Your Financial Health: Credit Scores and Stability

Your credit score and overall financial situation significantly influence the mortgage options available to you. Check your credit score before applying and take steps to improve it if necessary. A higher score can lead to better interest rates and more favorable loan terms. Additionally, prepare for potential interest rate increases by ensuring you can manage repayments if rates rise by 2%.

When selecting a mortgage, you must look beyond surface-level figures. These factors require comprehensive consideration to position yourself for a home loan that aligns with your long-term financial goals. The cheapest option isn’t always the best fit for your unique circumstances. Now that we’ve explored the key factors shaping your mortgage choice, let’s move on to effective strategies for comparing mortgage offers and securing the best deal for your situation.

How to Compare Mortgage Offers Effectively

Cast a Wide Net for Quotes

Recent research has explored developments that have slowed the pass-through of cash rate increases to the average outstanding mortgage rate between May 2022 and early 2024. This highlights the importance of obtaining multiple quotes to understand the current market conditions.

When you request quotes, be specific about your needs and provide consistent information to each lender. This approach allows for a fair comparison and gives you leverage when you negotiate terms.

Use Technology for Comparisons

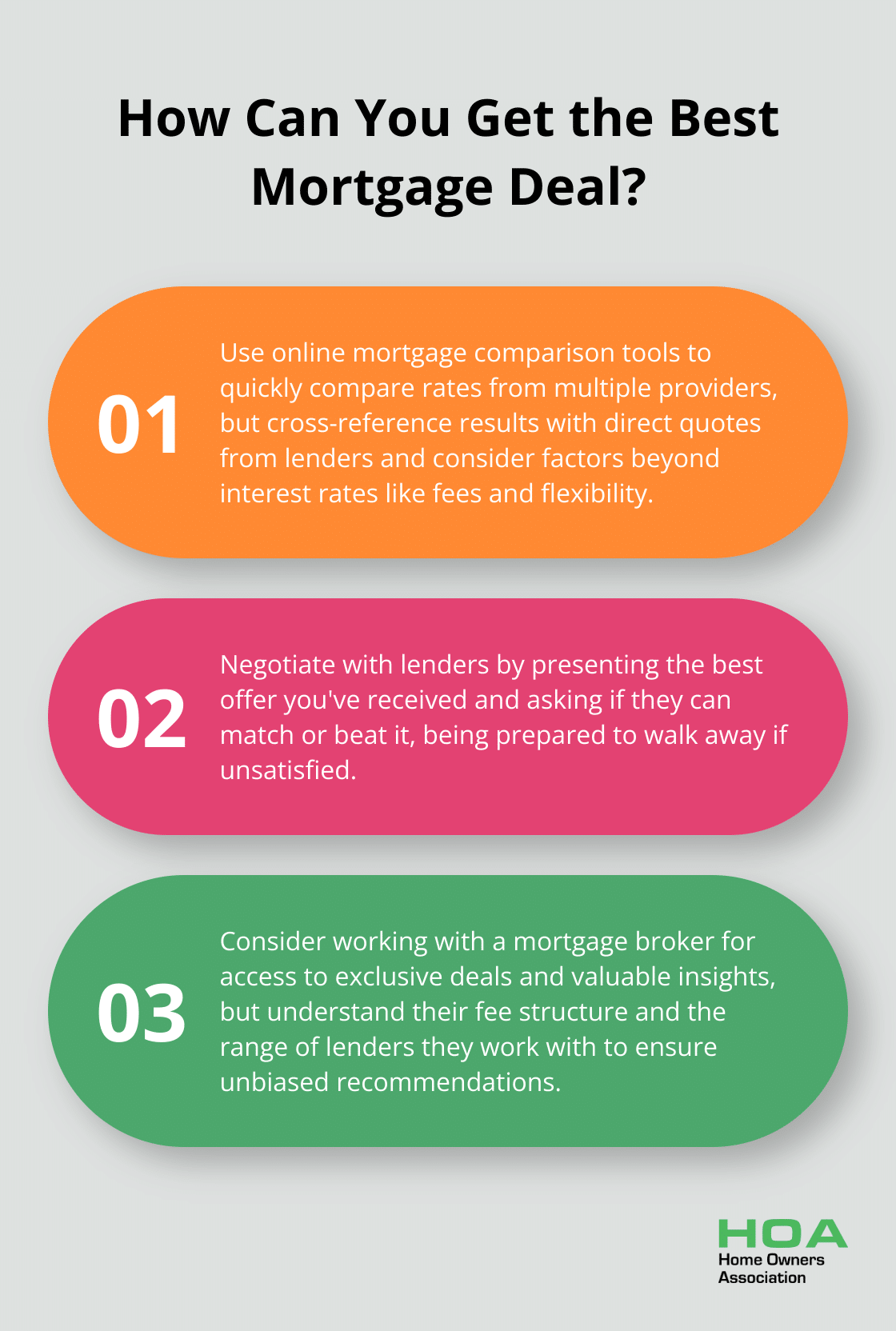

Online mortgage comparison tools have transformed how Australians shop for home loans. These platforms can compare numerous mortgage rates from multiple providers quickly. However, these tools may not include every available offer, and some may have commercial relationships with certain lenders.

You should use these tools as a starting point, but don’t rely on them exclusively. Cross-reference the results with direct quotes from lenders and consider factors beyond just the interest rate (such as fees, features, and flexibility).

Understand the True Cost of Your Loan

Look beyond the headline interest rate and focus on the comparison rate, which includes most fees and charges. For example, a loan with a lower interest rate might have a higher comparison rate when all costs are considered.

Pay close attention to upfront and ongoing fees. Application fees, valuation fees, and annual package fees can add thousands to your loan cost over time. Some lenders offer fee waivers or cashback deals, especially for refinancing, which can provide significant savings.

Negotiate with Confidence

Don’t hesitate to negotiate with lenders. The home loan market is highly competitive, and lenders often offer better terms to secure your business. If you have a strong credit score and stable income, you’re in an excellent position to negotiate.

Start by presenting the best offer you’ve received and ask if the lender can match or beat it. Be prepared to walk away if you’re not satisfied.

Consider Professional Guidance

While you can navigate the mortgage market on your own, working with a mortgage broker can provide valuable insights and potentially save you time and money. Brokers have access to a wide range of loan products and can often secure exclusive deals not available to the public.

Recent research highlights the importance of brokers in ensuring Australians are aware of all their options, including when Lenders Mortgage Insurance (LMI) can be the right choice. However, you should understand how your broker is compensated. Most receive commissions from lenders, which could influence their recommendations. Always ask about their fee structure and the range of lenders they work with.

Final Thoughts

Choosing the right home mortgage requires careful consideration of various factors. Interest rates, loan terms, and down payments significantly impact your financial future. Your credit score and overall financial health determine the options available to you, so it’s essential to understand these elements before making a decision.

Effective comparison of mortgage offers involves obtaining multiple quotes and understanding the total cost of your loan. Don’t hesitate to negotiate with lenders, as the competitive market often allows for better terms. Professional guidance from a mortgage broker can provide valuable insights and potentially save you time and money.

At Home Owners Association, we offer exclusive benefits and expert advice tailored to the Melbourne market. Our members access trade pricing and discounts, which can lead to substantial savings on home-related projects. We provide personalized guidance to help you make informed decisions throughout your homeownership journey, including valuable home mortgage tips.