At Home Owners Association, we understand that home improvements can be costly. Many homeowners are turning to small home renovation loans to finance their projects.

These loans offer a way to upgrade your living space without draining your savings. In this post, we’ll explore the various options for small home renovation loans and guide you through the application process.

What Are Small Home Renovation Loans?

Definition and Purpose

Small home renovation loans are financial products that help homeowners fund minor to moderate home improvement projects. A top-up is ideal if you’re happy with your current lender and need a relatively small to medium amount for renovations.

Loan Terms and Amounts

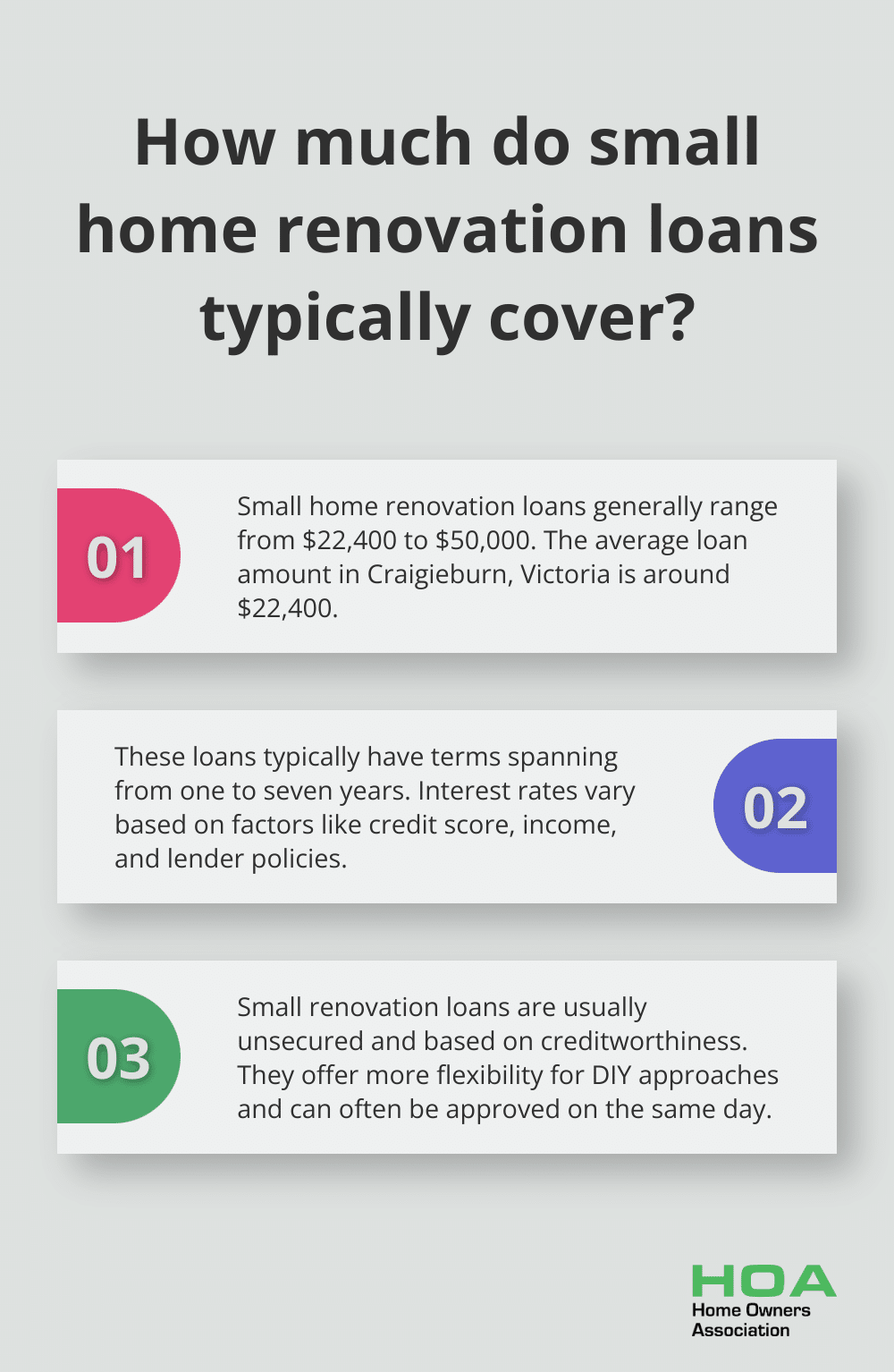

The terms for small home renovation loans usually span from one to seven years. Interest rates can vary widely based on factors such as credit score, income, and the lender’s policies. However, smaller loans for minor renovations are often much lower, with suburbs like Craigieburn in Victoria averaging around $22,400 per loan.

Differences from Other Financing Options

Small home renovation loans differ from traditional mortgages or large construction loans in several ways:

- They’re typically unsecured, meaning you don’t need to use your home as collateral.

- They’re based on your creditworthiness rather than your home’s equity.

- They offer more flexibility for DIY approaches.

These characteristics make small renovation loans accessible to newer homeowners or those in areas with stagnant property values.

Flexibility and Speed

A key advantage of small home renovation loans is their flexibility. Unlike construction loans (which require detailed plans and contractor involvement), these loans often allow for more DIY approaches. Many lenders offer same-day approval for amounts up to $50,000, providing quick access to funds for time-sensitive projects.

We’ve observed a growing trend of homeowners opting for these loans to upgrade their living spaces without the complexity of larger financing options. They’re particularly popular in affordable housing areas where residents want to enhance their properties rather than move.

As we explore the various types of small home renovation loans in the next section, you’ll gain a better understanding of which option might best suit your specific needs and circumstances.

Exploring Your Small Home Renovation Loan Options

Personal Loans for Quick Renovations

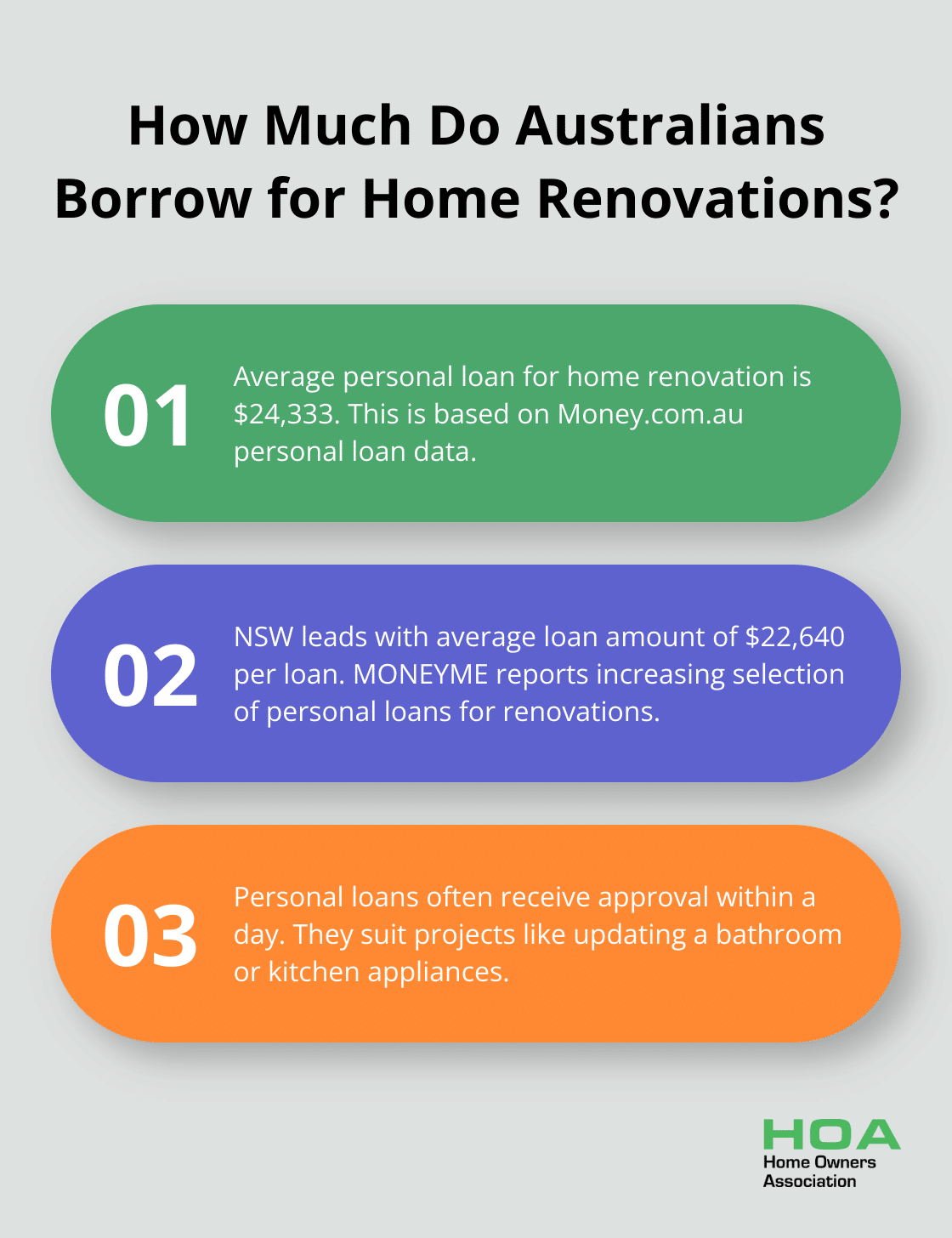

Personal loans stand out as a popular choice for smaller renovation projects. According to Money.com.au personal loan data, borrowers looking for a personal loan for a home renovation request an average loan amount of $24,333. These unsecured loans don’t require collateral and often receive approval within a day. While interest rates for personal loans typically exceed home equity options, they fall below credit card rates. They suit projects like updating a bathroom or kitchen appliances perfectly.

MONEYME reports that Australians increasingly select personal loans for home renovations. Loan amounts vary by location, with New South Wales leading at an average of $22,640 per loan. These loans offer fixed interest rates and predictable monthly payments, which simplifies budgeting for homeowners.

Home Equity Loans and Lines of Credit

Homeowners with significant equity might find home equity loans or lines of credit attractive. These secured loans often come with lower interest rates than personal loans because your home serves as collateral. The total amount a person can borrow depends on the value of the property and the equity they wish to keep in their home.

Home equity loans provide a lump sum, while lines of credit allow you to draw funds as needed. This flexibility proves particularly useful for ongoing or phased renovation projects. However, it’s important to note that you put your home at risk if you can’t repay the loan.

Government-Backed Renovation Loans

Some government programs offer renovation loans with favorable terms. For example, the Australian HomeBuilder grant provides eligible homeowners with funds for substantial renovations. While not a loan per se, this grant can significantly reduce the amount you need to borrow.

Additionally, some local and state governments offer interest-free loans for specific types of renovations (particularly those focused on energy efficiency or accessibility improvements). These programs can vary widely, so research what’s available in your area.

Credit Cards for Minor Touch-Ups

For very small projects or last-minute expenses, credit cards can serve as a convenient option. Some cards offer introductory 0% APR periods, which can benefit you if you can pay off the balance quickly. However, standard credit card interest rates typically far exceed other loan options, so consider this a last resort for larger expenses.

When weighing your options, compare the total costs, including interest payments and fees. Try to find the best fit for your renovation needs and financial situation. The right financing option can transform your renovation dreams into reality while maintaining solid financial footing.

As you consider these loan options, you’ll want to understand how to apply for a small home renovation loan successfully. The next section will guide you through the application process, helping you increase your chances of approval and secure the best possible terms for your project.

Applying for a Small Home Renovation Loan

Evaluate Your Financial Health

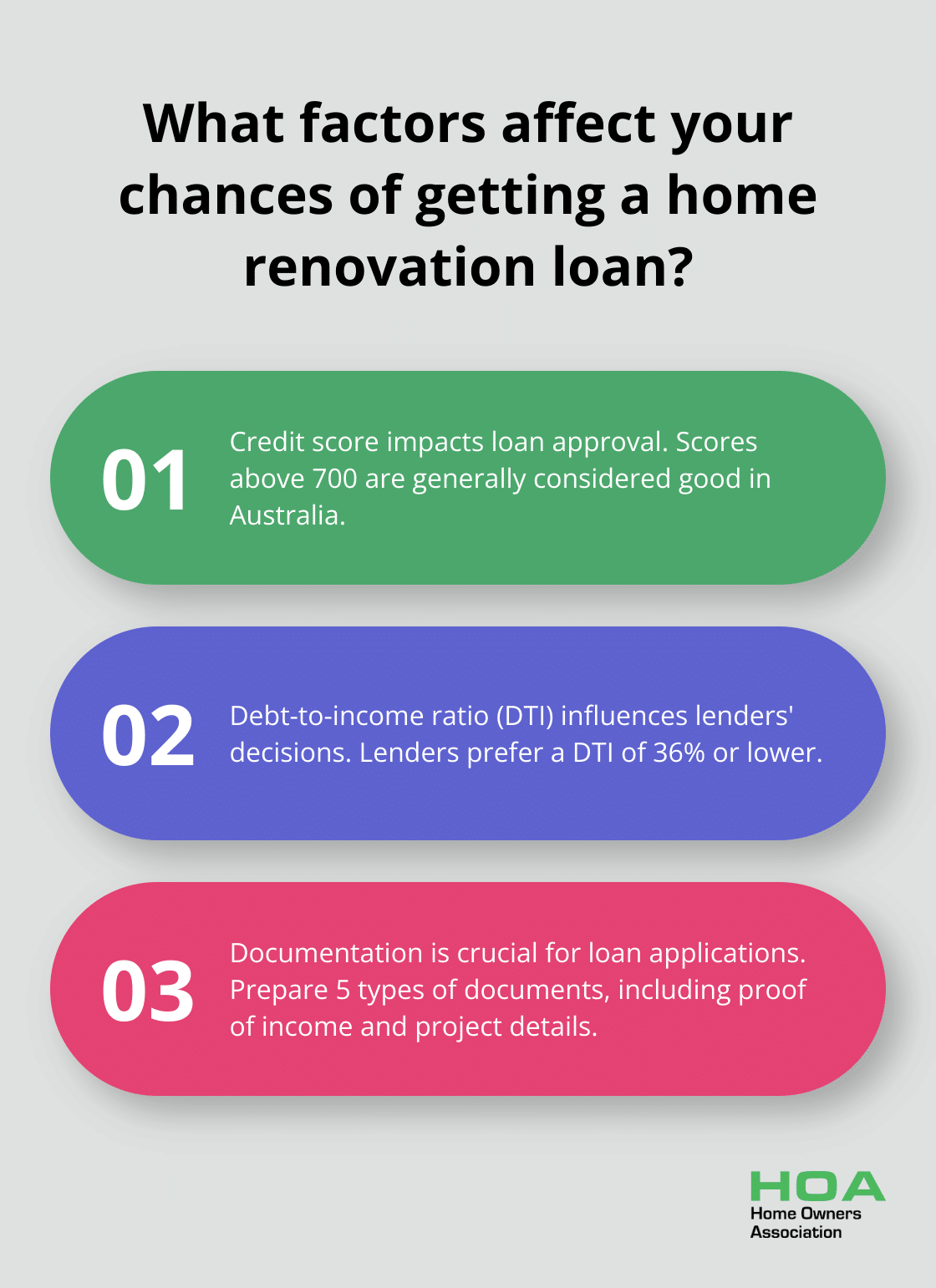

Before you apply for a loan, take a close look at your financial situation. Check your credit score through free online services or your bank. In Australia, credit scores typically range from 0 to 1,000 or 0 to 1,200 (depending on the credit reporting agency). A score above 700 is generally considered good and can improve your chances of loan approval and better interest rates.

Next, calculate your debt-to-income ratio (DTI). Your DTI is simply your total liabilities and debts divided by your gross annual income, calculated in order to reveal your full debt exposure. Lenders prefer a DTI of 36% or lower. If your DTI is high, pay down some existing debts before you apply for a renovation loan.

Prepare Your Documentation

Lenders require specific documents to process your loan application. Typically, you’ll need:

- Proof of income (pay stubs, tax returns)

- Bank statements (usually for the past 3-6 months)

- Proof of assets (savings accounts, investments)

- Identification (driver’s license, passport)

- Details of the renovation project (cost estimates, contractor quotes)

Have these documents ready in advance to speed up the application process. Many lenders now accept digital copies, so create a dedicated folder on your computer for easy access and sharing.

Compare Loan Options

With your financial health assessed and documents prepared, shop around for the best loan offers. Don’t limit yourself to just one type of loan or lender. Compare personal loans, home equity loans, and government-backed options.

Look beyond just the interest rate. Consider factors such as:

- Loan terms (length of repayment)

- Fees (origination fees, early repayment penalties)

- Flexibility (ability to make extra payments without penalty)

- Disbursement method (lump sum vs. line of credit)

Use online comparison tools to get an initial overview, but contact lenders directly for personalized quotes. Some lenders may offer better rates or terms based on your specific situation.

Maximize Your Approval Chances

To improve your chances of loan approval:

- Minimize credit inquiries in the months leading up to your application, as multiple inquiries can temporarily lower your credit score.

- Consider a co-signer if your credit is less than stellar. A co-signer with strong credit can significantly boost your approval odds and potentially secure better terms.

- Be realistic about the loan amount you’re requesting. Asking for more than you can reasonably afford to repay can lead to rejection.

- If possible, demonstrate the value your renovation will add to your home. Some lenders view this favorably, especially for home equity loans.

- Try to join a reputable homeowners association. Members often benefit from preferential rates and terms with partner lenders, thanks to established relationships in the industry.

Consider exploring energy-efficient home improvements that may qualify for government incentives, such as the Australian Government’s Small-scale Renewable Energy Scheme (SRES). In the 2023–24 Budget, the Australian Government allocated $1.3 billion to establish the Household Energy Upgrades Fund. These improvements can potentially increase your home’s value and provide long-term savings.

Final Thoughts

Small home renovation loans offer Australian homeowners various options to finance their projects. Personal loans provide quick approvals, while home equity products leverage property value. Government-backed programs and credit cards for minor updates complete the range of choices available to homeowners seeking to improve their living spaces.

Careful planning and budgeting form the foundation of a successful renovation. Homeowners should assess their financial situation, gather necessary documents, and compare offers from multiple lenders before applying for a small home renovation loan. This preparation increases approval chances and helps secure the best possible terms.

Well-planned renovations can increase property value, improve energy efficiency, and lead to long-term savings. The Home Owners Association offers valuable resources and exclusive discounts on renovation materials for Melbourne homeowners (who want to maximize these benefits).