At Home Owners Association, we understand that navigating the world of home loans can be overwhelming.

Securing the right mortgage is a crucial step in your homeownership journey. That’s why we’ve compiled expert home loan tips to help you make informed decisions.

In this guide, we’ll explore various loan types, factors affecting your application, and strategies to secure the best deal possible.

What Are the Main Types of Home Loans?

Understanding the different types of home loans is essential for making an informed decision. Let’s explore the most common options available in the Australian market.

Fixed-Rate Mortgages: Stability in Uncertain Times

Fixed-rate mortgages offer a consistent interest rate for a set period, typically between one to five years. This option provides peace of mind, as your repayments remain the same regardless of market fluctuations. For example, a 1-year fixed rate mortgage might have an interest rate of 6.49% p.a., while a 2-year fixed rate could be 6.24% p.a.

Variable-Rate Mortgages: Flexibility and Potential Savings

Variable-rate mortgages have interest rates that can change based on market conditions. While this introduces some uncertainty, it also offers the potential for lower rates when the market is favorable. The average rate on new variable rate loans increased by around 40 basis points less than the cash rate between May 2022 and December 2023, as reported by the Reserve Bank of Australia.

Split Loans: The Best of Both Worlds

Split loans allow you to divide your mortgage into fixed and variable portions. This strategy can provide a balance between stability and flexibility. For example, you might choose to fix 60% of your loan and leave 40% variable, allowing you to take advantage of potential rate drops while maintaining some predictability in your repayments.

Interest-Only Loans: Short-Term Solution for Investors

Interest-only loans require you to pay only the interest on the loan for a set period (usually up to five years). This option can attract investors looking to maximize tax deductions or first-time buyers seeking lower initial repayments. However, it’s important to note that your principal doesn’t decrease during this period, which can lead to higher overall costs in the long run.

Low-Doc Loans: Alternative for Self-Employed Borrowers

Low-documentation loans cater to self-employed individuals or those with irregular income streams who may struggle to provide traditional proof of income. While these loans often come with higher interest rates, they can be a viable option for those who don’t meet standard lending criteria.

When choosing a home loan, it’s important to consider your financial situation, future plans, and risk tolerance. Many homeowners find it helpful to consult with a financial advisor or mortgage broker to navigate these options and find the best fit for their needs. Now that we’ve covered the main types of home loans, let’s explore the factors that can affect your home loan application.

What Influences Your Home Loan Application?

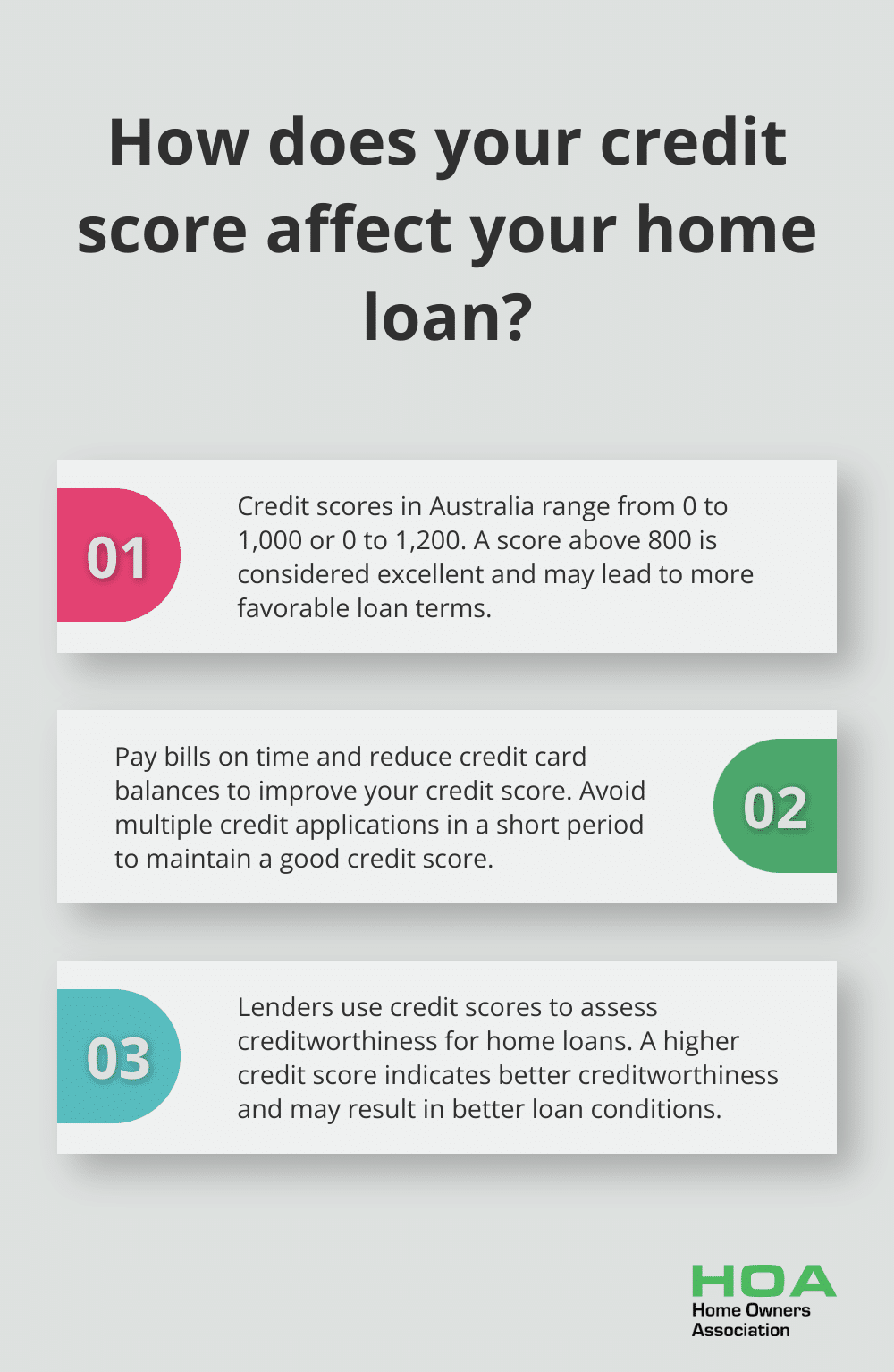

Credit Score: Your Financial Report Card

Your credit score plays a pivotal role in your home loan application. In Australia, credit scores typically range from 0 to 1,000 or 0 to 1,200 (depending on the credit reporting agency). A higher score indicates better creditworthiness. A score above 800 is considered excellent and may lead to more favorable loan terms. To improve your credit score, pay bills on time, reduce credit card balances, and avoid multiple credit applications in a short period.

Income and Job Stability: Proving Your Repayment Ability

Lenders require assurance that you can consistently meet your mortgage payments. They typically look for steady employment for at least two years. Self-employed applicants might need to provide additional documentation, such as business activity statements or tax returns for the past two years. Some lenders consider your industry and role when assessing job stability. A permanent position in a growing sector might be viewed more favorably than a contract role in a volatile industry.

Debt-to-Income Ratio: Balancing Your Financial Obligations

Your debt-to-income ratio (DTI) is a critical metric that lenders use to assess your ability to manage monthly payments. In Australia, around one-third of investors took out a loan with a DTI ratio above six in the June quarter of 2021, compared to around 20 percent of owner-occupiers. To improve your DTI, pay down existing debts or increase your income before applying for a home loan.

Deposit Size: Demonstrating Financial Discipline

The size of your deposit can significantly impact your loan application. A larger deposit not only reduces the amount you need to borrow but also demonstrates financial discipline to lenders. Try to save at least 20% of the property’s value as a deposit. This can help you avoid Lenders Mortgage Insurance (LMI) and potentially secure better interest rates.

Property Value and Location: Assessing the Investment

Lenders also consider the property you intend to purchase. They assess its value and location to determine the risk associated with the loan. Properties in desirable areas with strong growth potential may be viewed more favorably. Lenders may require a professional valuation to ensure the property’s worth aligns with the loan amount requested.

Understanding these factors can help you position yourself as a strong applicant and potentially secure better loan conditions. The next section will provide practical tips to help you secure the best home loan deal possible.

How to Secure the Best Home Loan Deal

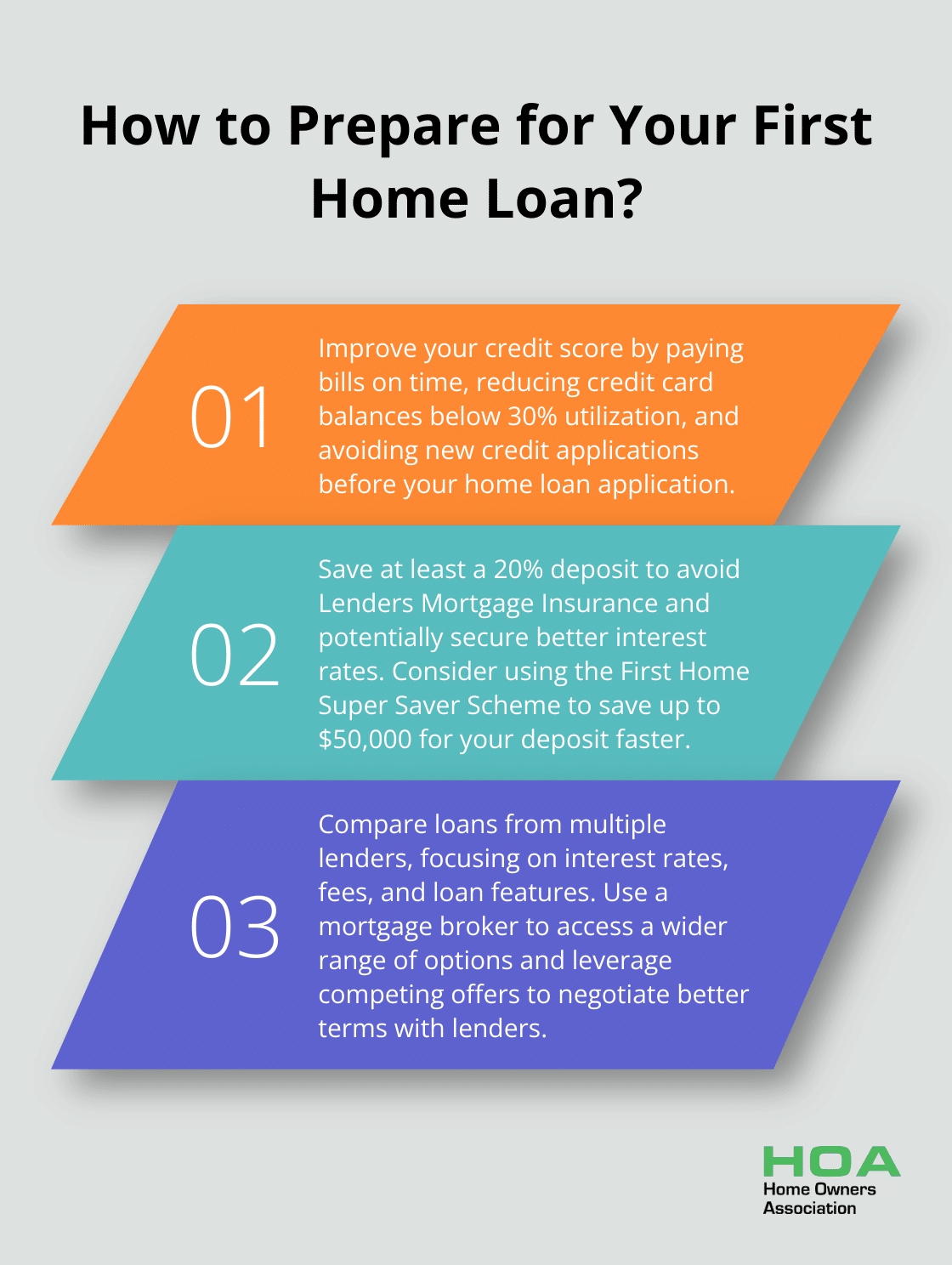

Improve Your Credit Score

Your credit score significantly influences your loan terms. Obtain a free credit report from a reputable agency. If your score needs work, pay bills on time and reduce credit card balances. Try to keep your credit utilization below 30% of your available credit. Avoid new credit applications in the months before your home loan application, as each inquiry can temporarily lower your score.

Increase Your Deposit

A larger deposit reduces your loan amount and shows financial discipline to lenders. Try to save at least a 20% deposit to avoid Lenders Mortgage Insurance (LMI). Set up automatic transfers to a high-interest savings account if you struggle to save. The First Home Super Saver Scheme helps first home buyers save a home deposit faster, allowing eligible buyers to withdraw up to $50,000 of voluntary contributions.

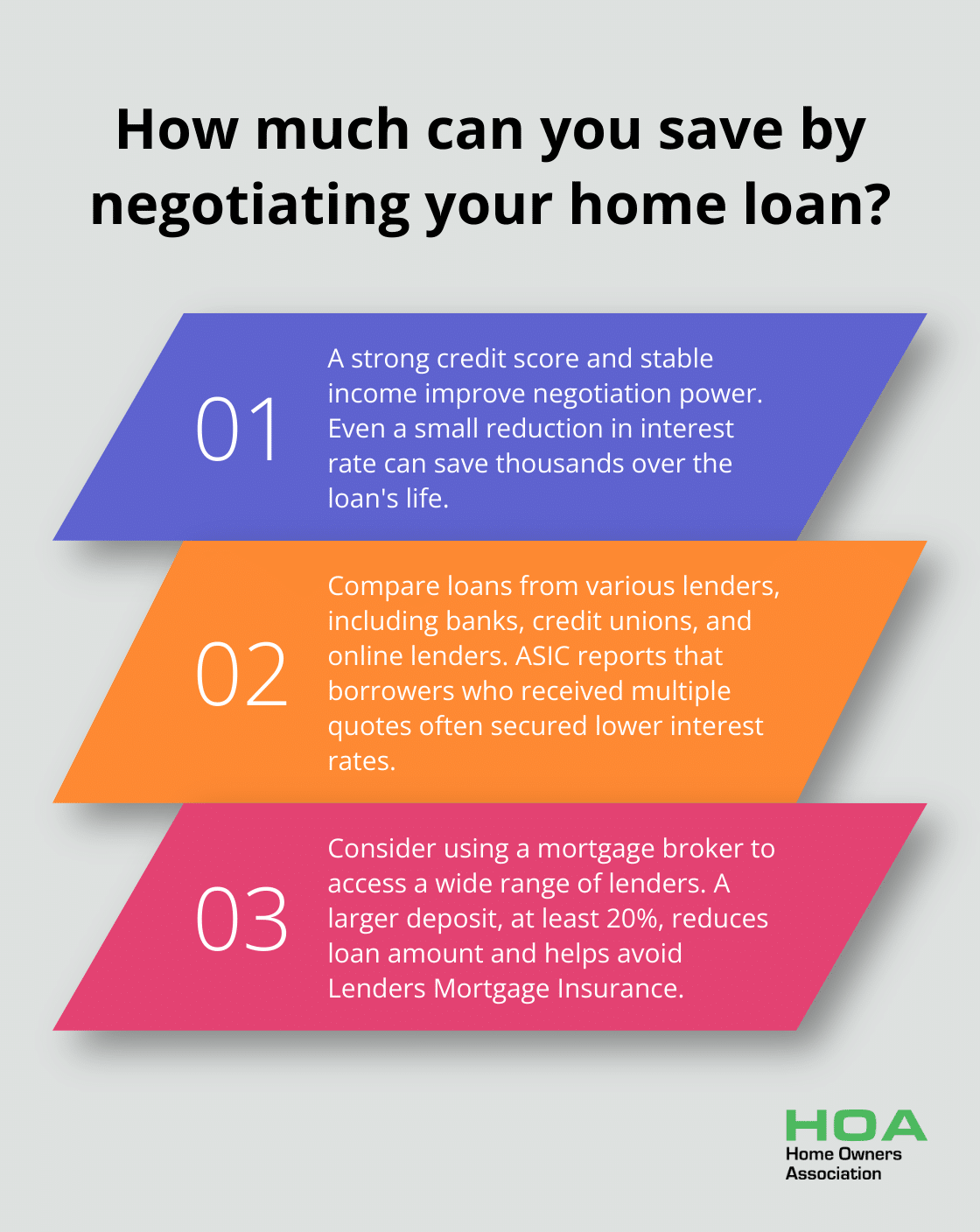

Compare Multiple Lenders

Don’t accept the first offer you receive. Research and compare loans from various lenders, including banks, credit unions, and online lenders. Focus on interest rates, fees, and loan features. The Australian Securities and Investments Commission (ASIC) reports that borrowers who received quotes from multiple lenders often secured lower interest rates.

Use a Mortgage Broker

A mortgage broker can be a valuable asset in your home loan search. They access a wide range of lenders and often secure better rates than you might find independently. Understand how your broker is compensated to avoid conflicts of interest.

Negotiate with Lenders

Don’t hesitate to negotiate with lenders. A strong credit score and stable income put you in a good position to ask for better terms. Leverage competing offers to negotiate lower interest rates or reduced fees. Even a small reduction in your interest rate can save you thousands over the life of your loan.

Final Thoughts

Securing the best home loan requires careful planning, research, and strategic decision-making. You must understand various loan types and factors influencing your application to navigate the complex mortgage world effectively. Our home loan tips emphasize the importance of improving your credit score, saving for a larger deposit, and comparing offers from multiple lenders to obtain favorable terms.

Professional advice can provide valuable insights when you face complex mortgage decisions. Mortgage brokers and financial advisors offer personalized guidance tailored to your specific circumstances. Their expertise can help you make informed choices aligned with your long-term financial goals.

Home Owners Association supports homeowners throughout their property journey. Our members in Melbourne receive trade pricing, discounts on materials, and expert advice for construction and renovation projects. These resources can help you make informed decisions and potentially save money on your home improvement endeavors.